Inspect the pack buyers see before you run your own scan.

This is the real Deal Pack surface in sample mode. Switch cases to see how the same verdict, maths, evidence, risks, and next move hold up across BTL, BRR, flip, HMO, and walk-away deals.

Inspect it like a buyer would.

The full sample is long on purpose, but the first judgment is simple: can someone understand the case, challenge the assumptions, and see what still needs proving?

Read the verdict first

The pack should say whether the deal is worth time, not just show a flattering yield.

Check proof labels

Observed, estimated, missing, and external-check items are kept separate so weak evidence stays visible.

Look for the next move

A useful pack should end with the action to take next: view, call, offer, strengthen proof, or walk away.

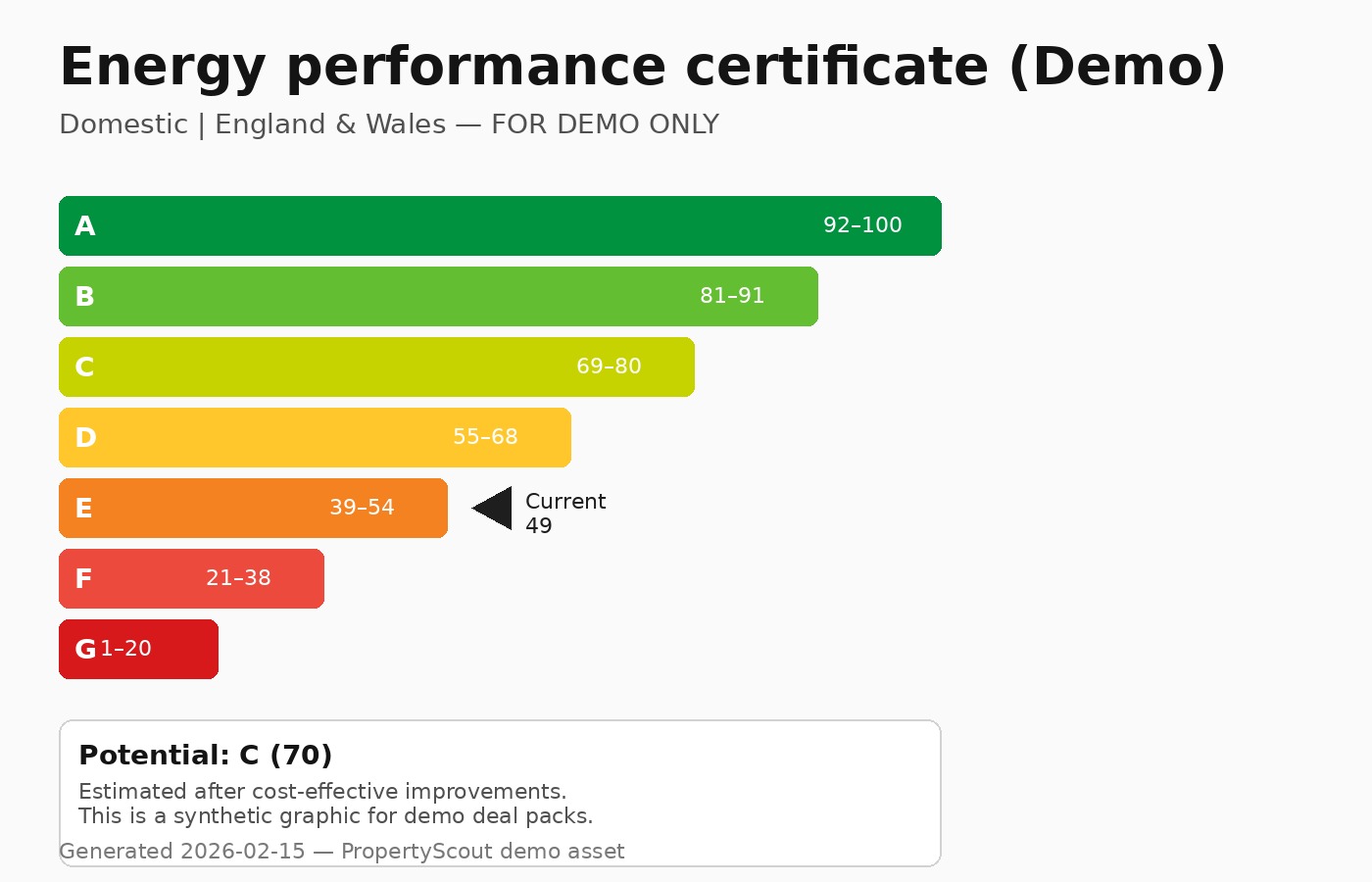

Cashflow-led HMO conversion candidate

Supporting scoresReadiness model, opportunity pressure, and offer-read score.Show detailHide detail

- No direct probate confirmation is established from the listing alone.

- No stronger motivation signal has been evidenced yet.

- Vendor timeline, occupancy status, and competing interest still need confirming.

- shared amenity upgrade (medium)

- bathroom capacity and finish (medium)

- Confirm Article 4 and licensing route before treating room-rent upside as real.

- Measure rooms, circulation, and shared amenity space on site before pricing the extra-room case.

- Price fire doors, alarm system, and escape-route works before increasing the entry.

- Confirm Article 4 and licensing route before treating room-rent upside as real.

- Measure rooms, circulation, and shared amenity space on site before pricing the extra-room case.

- Price fire doors, alarm system, and escape-route works before increasing the entry.

- Fire-safety upgrades may be more material than the photos suggest

- Kitchen and bathrooms may need compliance-led reworking rather than simple refresh

- Room circulation must be checked on the actual layout before any densification is priced in

- Article 4 and licensing checks can invalidate the HMO strategy completely.

- Fire safety, amenity, and egress upgrades may expand capex beyond the base hold budget.

- Void risk rises quickly if room sizes or finish land below local expectations.

- HMO potential

- Compliance first

- Measure rooms on viewing

- Confirm Article 4, licensing, and any planning relevance before moving beyond the BTL-backed offer.

- Measure all proposed rooms and shared amenity space on site before assuming the extra-room plan works.

- Price fire doors, alarms, escape routes, and any amenity upgrades before leaning on the HMO cashflow case.

- Keep the BTL fallback viable so the decision remains protected if the HMO route is blocked.

- Discount to local sold median with adequate sample depth

- Family-sized three-bed layout supports resilient tenant demand

- Cosmetic refurb scope rather than structural repositioning

- Offer ceiling and walk-away line are already modelled

- Confirm Article 4 and licensing route before treating room-rent upside as real.

- Measure rooms, circulation, and shared amenity space on site before pricing the extra-room case.

- Price fire doors, alarm system, and escape-route works before increasing the entry.

- HMO potential

- Fire-safety upgrades may be more material than the photos suggest

- Kitchen and bathrooms may need compliance-led reworking rather than simple refresh

- Room circulation must be checked on the actual layout before any densification is priced in

- Article 4 and licensing checks can invalidate the HMO strategy completely.

- Fire safety, amenity, and egress upgrades may expand capex beyond the base hold budget.

- Void risk rises quickly if room sizes or finish land below local expectations.

- Is the property within Article 4 or any local policy area that affects HMO use?

- Has the branch seen investor or HMO interest already, and what feedback came back on layout?

- Any history of extensions, loft works, or layout changes that would affect licensing or building-control sign-off?

- Can the branch confirm current occupancy, vendor timeline, and any works done in the last five years?

- Are there any issues likely to affect lender appetite if the asset is held as a standard BTL?

- 1) Validate the policy route firstCheck Article 4, local licensing, and planning relevance before you spend time modelling room rents.

- 2) Measure the layout on siteConfirm room sizes, shared amenity space, and circulation before assuming the extra-room plan is compliant.

- 3) Price the fire-safety scopeDoors, alarms, escape routes, and amenity upgrades should be costed before the HMO upside is taken seriously.

- 4) Keep the BTL fallback front and centreIf the compliance route weakens, the property still needs to make sense as a straightforward hold at the packaged offer.

The sample separates evidence from assumption.

The point is not to make every deal look exciting. It is to show what is observed, estimated, missing, and still needs checking.

Decision posture

The real edge is optionality: viable single-let fallback with materially stronger cashflow if the HMO case clears.

Proof view

The upside case is meaningful, but it depends on licensing, compliant layout, and fire-safety scope holding up.

Next move

Validate council stance, rooming logic, and compliance cost before treating the higher cashflow case as real.

Use the same pack standard across hold, BRR, flip, HMO, and walk-away cases.

Run free preview scanRun this standard on your own area.

The preview scan shows the ranked queue first. Full Deal Packs open after the trial starts.

Run free preview scan